Tax benefit on your home loan interest comes under section 24b and applies to properties you have purchased whether for a residential or as an investment

As you all are aware that a taxpayer can claim the deduction towards his or her home loan EMIs which consists of principal and interest both. In this article, I am demystifying the tax benefit on your home loan interest. Tax benefit on your home loan interest comes under section 24b and applies to properties you have purchased whether for a residential or as an investment. Let us understand in detail how this benefit is calculated:

What is the maximum amount of interest deduction?

The maximum amount which you can claim as a deduction from your other taxable income i.e. say salary is Rs 2 lakh per annum. But if you would have given your property on rent then there is no limit to the amount of interest you can claim against your rental income but there is a limit of Rs 2 lakh against setting off that interest against your salary or other income.

What is the Impact of this Rs. 2 lakh limit?

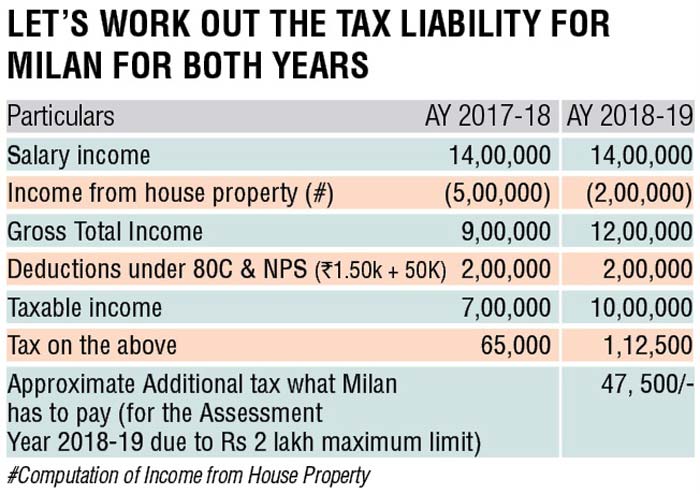

Let’s take an example of Milan, who earns a salary of Rs 14 lakh for the financial year 2016-17 i.e. the assessment year 2017-18 and financial year 2017-18 i.e. the assessment year 2018-19. He owns two houses:

Property A – Using it as a self-occupied and for this house, he pays an interest of Rs 2.8 lakh

Property B – He has rented it out for Rs 5 lakh annually and pays interest of Rs 6.50 lakhs

He has also invested in a mutual funds ELSS for Rs 1.5 lakh and NPS of Rs. 50,000.

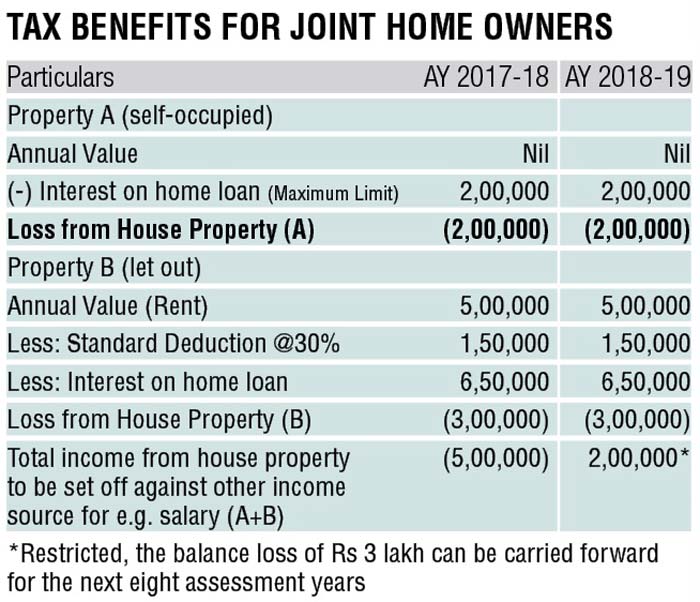

Tax benefits for joint homeowners!

In our above example, assume that Milan is married to Anjali and both of them are the joint owners of their both the properties. In this scenario, the benefit of interest as a co-borrower will be given to both of them individually to an extent of Rs 2,00,000 each which is a huge benefit in case Milan would have purchased both the properties in his name only. It has to be applied in the same ratio as what they have for their ownership share in respective properties.

"Home loan")

)

)

)

)

)

)