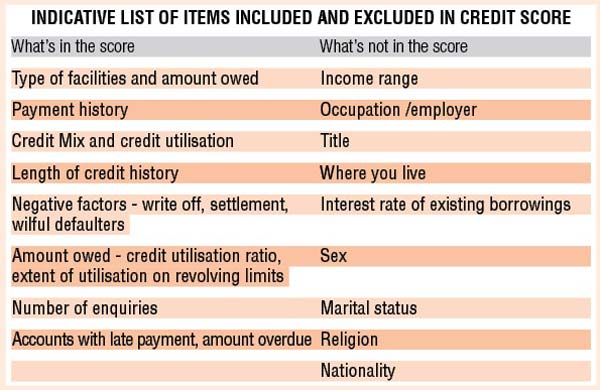

The credit report is a compilation of borrowings, behaviour of repayment, enquiries made, demographic data of residential address, office address, trend of repayments, unique ID numbers (like PAN, driving license and Aadhar)

Till a few years ago, loan processing was more subjective in nature and inconsistent. However, with digitisation, we are in a whole new world of instant credit and insta-loans. Credit processes coupled with technological initiatives has transformed the entire customer experience ecosystem with institutions relying more on credit reports generated by credit information companies (CIC).

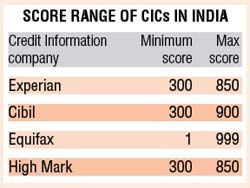

These CICs are regulated independent agencies which collate and aggregate customer data. At present, there are four credit rating agencies which provide ratings for individuals - CIBIL, Experian, Equifax and CRIF High Mark.

CIC generates a summarised report of all the borrowing facilities in the format known as credit report. The credit report is a compilation of borrowings, behaviour of repayment, enquiries made, demographic data of residential address, office address, trend of repayments, unique ID numbers (like PAN, driving license and Aadhar), of an individual, reported over a period of time.

Credit Score can be compared to marks scored in the school report card. However, unlike school reports, your credit score is calculated basis algorithms, giving different weightages and relevance against each parameter of the credit report. The score evaluates your ability as an individual or an organisation to fulfil financial commitments.

Credit reports and credit score help lenders gauge the repayment ability and willingness of a borrower on the basis of his past repayment behaviour. Scores help banks in making fair credit decisions, ensure faster processing, and optimise risks, basis the profile of customers. Credit report usage is not limited to just banks or financial institutions, but also visa processing companies, insurance companies, telecom companies, and most importantly your employers can use credit reports to know the profile of applicants. So if you plan to go abroad for further studies or simply travel, your credit report is crucial.

Credit reports and credit score help lenders gauge the repayment ability and willingness of a borrower on the basis of his past repayment behaviour. Scores help banks in making fair credit decisions, ensure faster processing, and optimise risks, basis the profile of customers. Credit report usage is not limited to just banks or financial institutions, but also visa processing companies, insurance companies, telecom companies, and most importantly your employers can use credit reports to know the profile of applicants. So if you plan to go abroad for further studies or simply travel, your credit report is crucial.

Lenders use credit reports for client's identification, account behaviour and enquiries of customers. Therefore, it becomes imperative as a customer to know what is included in the report and what is excluded. Variables used for calculation vary from one company to another, basis their score models.

How can consumers improve their scores?

The good news is that it is possible to improve your score – all you need to do is start taking concrete steps right away to improve the score. Here are some suggestions that can have a positive impact on your credit score.

Check your credit report: This is to ensure the correct listing of your loan accounts, correct reporting of payments and that the amount owed against each open account is correct. Reduce burden on revolving limits and use those responsibly : Even a single late payment, whether it is for loan or your credit card, has a negative impact on your score. Set up payment reminder for the credit card and bills due.

Use the right type of borrowing mix needs: For example, use credit cards for smaller purchases, car loan for car purchase and home loan for housing requirement. Problems crop up when consumers borrow short term loans for long term needs.

With these suggestions in place, it can take 6-18 months to improve your credit score. After all a good credit score is worth the patience and discipline, ensuring low interest rates and better credit terms.

There are many myths surrounding the issue of credit reports. Firstly, once a facility is closed, history of loan repayment too is removed. However, the fact is that credit report includes history of closed loans. All older history of good and bad repayments is included in the report. Another myth is that once defaulted and reported on bureau, an individual is not eligible for loans from banks. The fact is that credit report is one of the tools of assessment. Bankers look at the larger picture of overall profile and take a call on justified delays. And finally, credit score of joint applicant /guarantor is not impacted in case of default. However, credit score of applicant, co-applicant and guarantor is equally impacted due to adverse performance on bureau for particular facility.

The writer is senior group president – retail and business banking, YES Bank

"Credit Report")

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)